This article was reviewed by Chris Singer, CFP®.

You’ve been paying into CPP all of your working life—or at least since you were 18. Now, with retirement around the corner, you’re excited to finally get to receive that first payment from your government pension.

Unfortunately, not a lot of people know how this pillar in Canadian retirement planning works. They don’t exactly teach it in school (even if they did, that was about 40 years ago).

And worse, sometimes in their excitement, people make mistakes that can be costly in the long run, like taking CPP too early.

So when you’re putting together your retirement plan, it’s important to have an idea of what CPP is and how you can properly use it so you’re not making mistakes that could have been easily avoided.

What is CPP?

The Canada Pension Plan—or CPP—is a retirement pension that’s paid monthly by the federal government of Canada to replace a certain amount of your average work income, up to a maximum limit. Once you start taking it, it’s paid for life.

The social program, which was created in 1965, is a contributory, earnings-based program that forms one of the two pillars of Canada’s retirement income system, along with OAS (Old Age Security).

Is CPP taxable?

CPP counts as income and as such is taxable. You can elect to have the tax taken off of the benefit. We typically recommend you have 20% of your CPP payment, withheld for taxes, though that depends on two factors:

- What other income sources you have and whether those have tax taken off of them (like OAS, pensions, RRIF payments…)

- On your preferences and if you like to have a tax bill later once a year or to pay income tax on a regular basis.

How does CPP actually work?

Now that you understand the basics of what the Canada Pension Plan is, let’s take a look at how it works.

What are CPP contributions?

How it works is pretty simple: anyone who is employed, over 18 years of age and receives a salary must make contributions to CPP until the age of 65. Your employer also contributes to CPP on your behalf (which, if you’re self-employed, is you).

Who manages CPP?

Who manages CPP?

Who manages CPP?

Who manages CPP?The Canada Pension Plan Investment Board (CPPIB) manages the contributions—with, as of June 30, 2021, over $519 billion in assets under management on behalf of 20 million Canadians—and reports annually to Parliament through the Minister of Finance to make sure the program is sustainable in the long-term.

The most recent triennial report (2019) indicated that CPP would be sustainable for at least 75 years. The Chief Actuary of Canada concluded that “despite the projected substantial increase in benefits paid as a result of an aging population, the Plan is expected to be able to meet its obligations throughout the projection period.”

Who is eligible to receive CPP?

Everyone aged 60 and over is eligible to receive CPP. However the amount you’ll get will depend on a few factors, which I’ll outline below.

The standard age to start receiving CPP is 65 years old but you can choose to start as early as age 60 (and receive a smaller monthly amount) or as late as age 70 (and receive a larger monthly amount). We’ll cover why you would want to do one or the other later in this article.

With all this in mind, let’s now move and take a look at the question on most people’s minds: how much can you actually get from CPP?

When will you receive CPP?

Your CPP benefits are paid on the last Thursday of the month that’s not a stat holiday. Here’s a list of the CPP payment dates for 2022. You can add them to your calendar.

How much will you receive from CPP?

Now that I’ve covered what CPP is and how it works, let’s take a look at how much you can actually get each month from the benefit (source).

For 2021, the maximum monthly amount you could receive as a new recipient starting the pension at age 65 is $1,203.75. The average monthly amount in June 2021 is $619.68. Your situation will determine how much you’ll receive up to the maximum.

The maximum CPP goes up each year with inflation. Historically about 1.15%.

Like I already said above, how much you’ll actually get from CPP is based on several factors:

How long (and how much) you’ve contributed to CPP

How much you’ve earned

How old you are when you start taking CPP

Want to know how much your CPP payments will be? The government of Canada has a CPP calculator for you.

How long you’ve contributed to CPP

How long you’ve contributed to CPP is calculated by your Number of Contributory Months (NCM).

Your contributory period starts the month after you turn 18 (or January 1966, whichever is later) and ends either the month you turn 70 or the month before you start taking your CPP pension. It will also exclude any month that you received CPP disability benefit.

There are two dropout periods that act as a kind of grace to help you get the most out of CPP:

- Child Rearing Provision

- General Dropout

In order to get the maximum CPP, you need to have contributed to the pension for at least 39 years of employment.

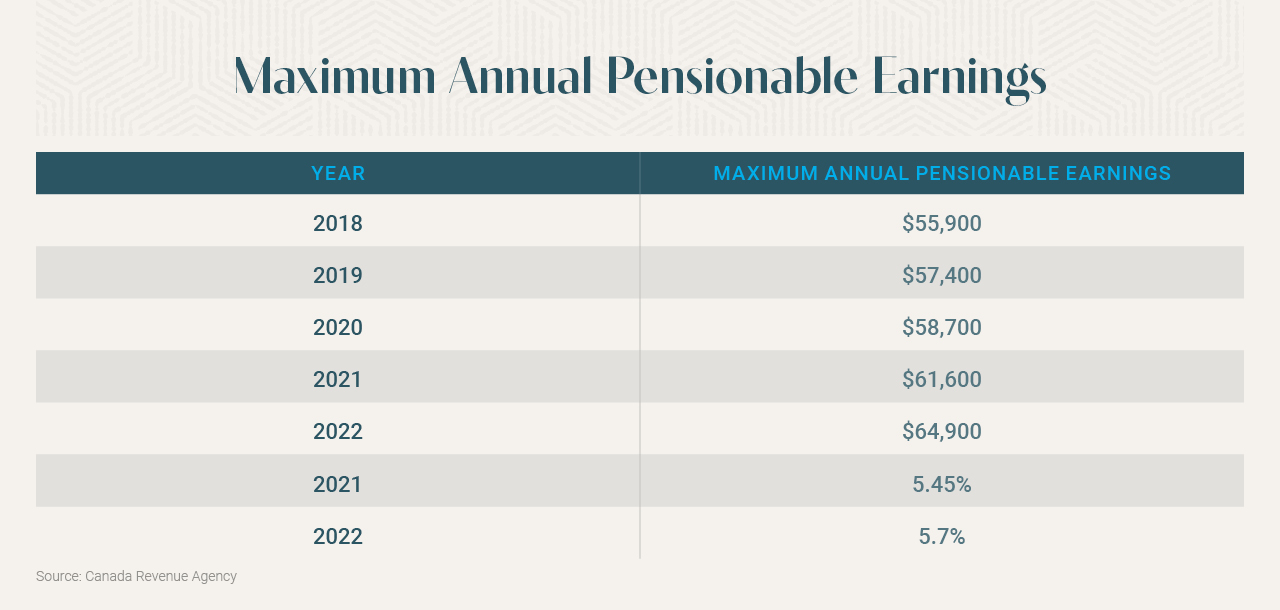

The maximum you can contribute to CPP

The most you can contribute to CPP is referred to as the Yearly Maximum Pensionable Earnings (YMPE).

This number is set and adjusted every year by the Canadian government based on the average wage in Canada.

This number is set and adjusted every year by the Canadian government based on the average wage in Canada.

The Enhanced CPP also introduces a second ceiling for those earning more than the YMPE, adding an additional 8% in the contributions on their income that’s between $57,400 and $65,400 in today’s dollars.

When do you start taking CPP?

The standard age for taking CPP and getting your full benefit is 65.

Like I said, you can choose to take CPP early starting at age 60 in return for a reduction in benefits equivalent to 0.6% for every month prior to your 65th birthday which adds up to a decrease of 7.2% a year or 36% total by the time you turn 65 (0.6% x 60 months).

Conversely, you can wait until you turn 70 to start taking CPP in return for an increase in benefits equivalent to 0.7% for ever month after your 65th birthday, which adds up to an increase of 8.4% per year or 42% total by the time you turn 70 (source).

Should I take CPP early or delay?

Some financial planners encourage retirees to take CPP early because ages 60 to 70 tend to be your higher spending years in retirement and, the argument goes, it’s beneficial to have that supplementary income.

For us, the penalty for taking CPP before 65 is so stiff, we usually don’t recommend to take it early (we usually can make up that supplementary income through your investments).

Another big question we consider is: how long someone will live? Typically, we’ve seen that by the time someone reaches their mid 70’s, they will outpace taking CPP prior to age 65, which is another big reason to wait.

The table above illustrates the benefits of waiting to take CPP. Even when we project a 5% return—which would benefit taking those payments early—by age 74, you’ve gotten more by waiting til 65 to start taking it. If you delay CPP until age 70, you can see that within 9 years (age 79), you’ve gotten more than somebody who started at 60 and has been receiving payments for 19 years.

Based on the table above, this graph shows you the total you would receive from CPP, based on whether you take it early at age 60, take it at 65 or defer until age 70 (these calculations are hypothetical in nature, do not reflect actual investment results and are not guarantees of future results).

There are a couple of cases where it might make sense to wait until you’re 70 to start taking CPP:

- If you’re still working past age 65 (or pulling an income from your business)

- If you sold your business and are receiving a payout

- If you’re a widower and receiving a survivor pension from CPP

As a rule of thumb, you should look at what your need for income is, the sources you have available, how you’ll be taxed on those sources and whether that taxation will drop.

How to apply for CPP

Service Canada recommends that you apply for your pension at least six months before you want your first CPP payment to begin. If you’re ready to start taking your Canada Pension Plan benefits, there are a couple of ways you can apply:

- Online on the Service Canada website

- By phone by calling 1-800-277-9914 if you’re in Canada or the United States or 613-957-1954 if you’re in any other country (Service Canada will accept collect calls)

- In person at a Services Canada office near you

Peace of mind comes from planning

CPP is a central source of income for every Canadian. There are a lot of different ways to make it fit in your retirement plan so you can retire your way.

The good news is: you don’t have to figure this out on your own. We’ve put together a free worksheet to get you started with everything you need to plan for a successful retirement.

Because retirement is the journey of your life and you should be free to enjoy it.<